Employee ownership trusts: the pros and cons

Shareholders looking to dispose of their companies in a tax efficient way may have noticed that one potential route promises to be entirely tax free – the sale of the company to an employee ownership trust. Can it really be that easy? The advantages and disadvantages of deciding to embark on this course are examined below.

The relief

The relief was introduced in 2014 and companies such as Riverford Organics and Richer Sounds have been transferred to employee ownership trusts to take advantage of it.

Providing all the conditions for the relief are satisfied, the sale of the shares to the trust will be deemed to occur at a value which produces neither a gain nor a loss for the seller for capital gains tax purposes. In other words, there is no tax.

The conditions

The main conditions for the relief to apply are:

- the seller must be an individual or a trust, not a company;

- the shares must be ordinary shares, not preference shares;

- the company must be a trading company, or the principal company of a trading group, which broadly means that at least 80% of the activities must be trading activities;

- the trust must acquire a controlling interest in the company (which it did not previously possess); and

- after the sale, at least 60% of the employees must not be significant shareholders.

The trust

The trust which acquires the shares has to satisfy the following main rules:

- the trust must generally be for the benefit of all employees of the company or group, who must benefit on the same terms, although employees who have worked for the company or group for less than a year can be excluded, and the trust can permit funds to be applied for charitable purposes;

- the trust must exclude employees who in the last 10 years have owned 5% or more of the shares in the company (or of any class of shares in the company), or who on a winding-up would be entitled to 5% or more of the assets of the company, and anyone connected with such employees must likewise be excluded;

- the trust can allow employees’ entitlements to vary with their remuneration, length of service or hours worked, but all eligible employees must have some entitlement; and

- the trust cannot make loans to the employees.

The pros

Some of the advantages of choosing to sell a company to an employee ownership trust are as follows:

- the tax advantages: not only is the sale free of capital gains tax for the seller, but eligible employees can be paid bonuses of up to £3,600 per year free of income tax (although surprisingly not free of national insurance contributions);

- the trust is a ready-made purchaser: ordinarily sellers needs to find a buyer in order to sell their company – maybe the existing management or a third party purchaser. By creating the trust, the sellers can sell their shares without going through this step, almost as if by magic;

- succession planning: likewise, the trust removes the requirement for business owners to spend time searching for a suitable buyer whose values match those of the existing owners, the employees and the company ethos. The trustees can include the existing owners, resulting in a seamless transition and minimal disruption to the day to day running of the business;

- the price: some magic applies here too. With many sales, negotiating the sale price is the central stumbling block. With a sale to the trust, the price is often arrived at by obtaining a professional valuation of the company, and selling at that value (which might include an earn-out element). The trustees must satisfy themselves that they are not overpaying for the company but the process should be less fraught;

- benefiting the staff is a good thing: most people would think that placing the ownership of a business in a trust for the employees is a form of philanthropy. Also, the employees feel valued and this is conducive to a happy working environment for both the employees and the company;

- retaining and attracting staff: with the company owned by an employee trust, and possibly coupled with the introduction of an employee share option scheme for sought after individuals, staff should see their career progression enhanced and it should be easier to both retain and attract the most skilled and ambitious employees in their field;

- the sellers can remain very involved in the business: they can generally retain a minority shareholding and remain as directors receiving market rates of pay, providing the conditions described above are satisfied. Of course, sellers can remain involved in the business in third party sales and management buy-outs too, but their influence is likely to be less in such structures.

The cons

With upsides, there are always downsides. Some of the disadvantages of choosing to sell a company to an employee ownership trust are as follows:

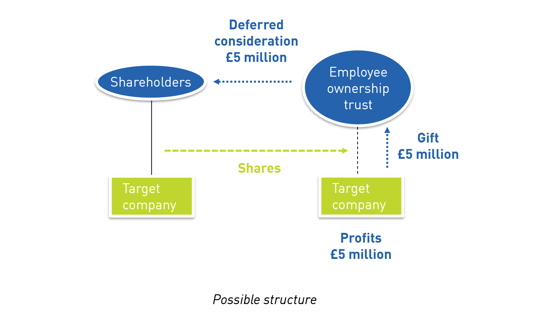

- getting cash upfront: with a normal sale a purchaser will often make an immediate cash payment and further payments based on the future results of the company – an earn-out. An employee ownership trust starts with no money and so, unless the company has surplus cash, its ability to make an immediate payment is likely to be limited to the amount it can borrow, which may not be that great. The sellers are therefore likely to receive the bulk of their proceeds on a deferred basis, payable out of future profits of the business, when (and if) these are received by the trust. So the sale to an employee ownership trust may be more risky;

- the trust is in control: although the sellers can have a large degree of influence after the sale, ultimately the trust has a controlling interest in the company. Even if the sellers control the trust (for instance by being the directors of a company which is the corporate trustee of the trust), they must exercise that control in the best interests of the beneficiaries of the trust – the employees. There is no escaping the fact that, after the sale, the company is largely owned by an employee benefit trust, operating for the benefit of the employees;

- the tax complications: although a sale to an employee ownership trust is generally considered to be tax advantageous, the position in practice is more complicated;

- the tax relief on the sale of the shares will not apply to any ‘earn out’ element of the consideration – for instance if the sellers are to receive further payments the amount of which depends on the future performance of the company. Such payments may be partly taxable when received;

- the tax relief on the sale of the shares will be lost if the trust sells its controlling interest in the company before the end of the tax year following the sale. The same is true if the company ceases to be a trading company before the end of the tax year following the sale;

- if the trust sells its controlling interest in the company, or the company ceases to be a trading company, after the end of the tax year following the sale, the trust itself will be subject to capital gains tax. Since the trust is deemed to acquire the company at the price the sellers paid for it, this will result in the trust paying tax on a larger gain than it actually made. It may be possible to circumvent this charge by setting up the trust offshore, although this adds to the complexity of the structure;

- the trust will have to pay stamp duty on the acquisition of the company (at ½%).

The conclusion

Sales to employee ownership trusts are not too good to be true. There are complications and they will not suit all sellers or all companies. But they are attractive transactions in many circumstances and they should be considered by anyone currently thinking of selling a company.